AGB 2024.6 - IDEXX Laboratories (IDXX)

Diagnostics for Companion Animals

Subscribe to AGB - One analysis of a good business in each issue.

IDEXX Laboratories

“Our strategy as a company is to be able to drive the relevant use of diagnostics through all life stages of a pet's life, because we think it's just so effective at uncovering disease and providing the veterinarian with the tools to identify what the best possible treatment is. And so, we've seen a steady increase in diagnostics both from an adoption and utilization standpoint.” - CEO Jay Mazelsky at IDEXX’s 2023 Investor Day

IDEXX is the leading provider of diagnostics instruments, tests and services for the companion animal veterinary industry. The company serves veterinary practices by providing the necessary tools to diagnose illnesses and diseases. Diagnostics are becoming an increasingly larger contributor to the financials of their customers. As IDEXX’s diagnostic instruments and services become an essential part of veterinary practices, these customers tend to also adopt the company’s software offerings like practice management (ezyVet, Neo), order management (VetConnect Plus) and customer engagement (Vello).

IDEXX has three segments, the Companion Animal Group (CAG), Water and Livestock, Poultry and Dairy (LPD). Over 91% of 2023 revenues were from the CAG segment, so the other two segments don’t get as much attention because of their minimal impact to the financial model. We’ll go over them quickly.

Water was 4.6% of 2023 revenues and has the highest margins of the three segments at 69% gross margins and 44% operating margins. This segment is comprised of water testing instruments, mainly to detect the presence of coliform bacteria and E. coli in water. These tests are mainly used by government labs and utilities to test drinking water to comply with regulatory standards for over 2.5B people. The water testing segment commands the company’s highest level of customer retention at 99+%.

LPD was 3.3% of 2023 revenues and has the lowest margins at 54% gross margins and 8% operating margins. This segment provides instruments, tests and services for livestock, poultry and milk safety. The three main tests are for Bovine Viral Diarrhea Virus, Porcine Reproductive and Respiratory Syndrome and African Swine Fever. China is a large part of the international portion of this segment, which has been a headwind recently.

CAG was 91.6% of 2023 revenues and has seen improving operating margins over the past 10 years as this segment has benefited from increasing scale and higher contributions from consumables. CAG is broken down into smaller categories but the main ones are instruments, consumables, rapid assay products (SNAP), reference lab services and software.

Within diagnostics, IDEXX started out by mainly selling SNAP rapid assay tests (10% of 2023 CAG revenues). These are single-use test-kits for certain diseases including Lyme disease, heartworm infection, feline immunodeficiency and leukemia and others. Most SNAP tests can be run without the use of instruments, but they can also be further analyzed using an instrument like the company’s SNAP Dx/Pro Analyzers. Rapid assay test revenues have increased over time but are shrinking as a % of the CAG segment due to outpaced growth in consumables used for in-clinic instruments.

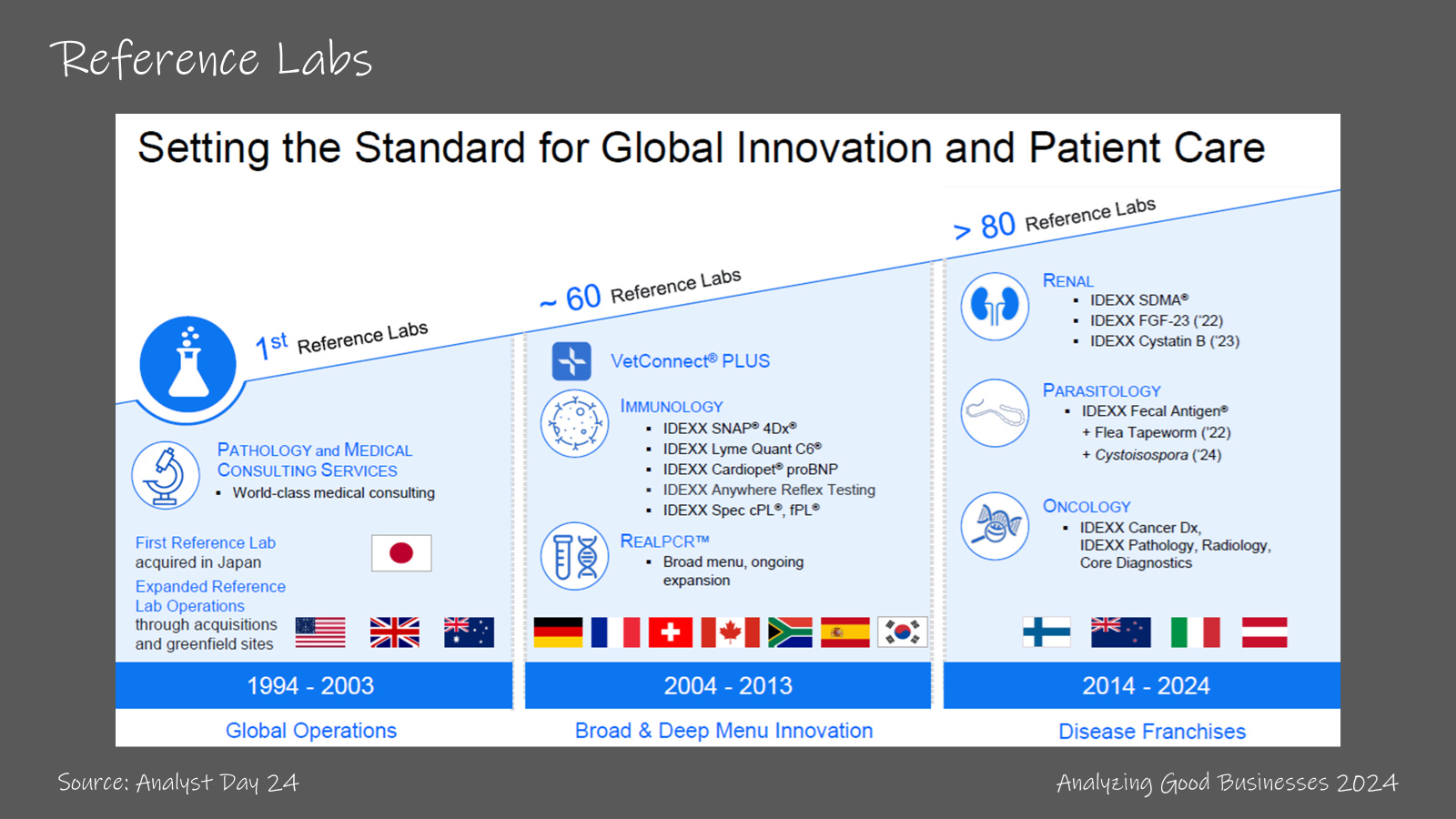

The company then evolved to offer reference lab services (38% of CAG revenues). This is where samples are sent from a veterinary practice or hospital to one of IDEXX’s 80+ labs around the world, usually through same-day or an overnight delivery service. Certain lab tests can also be run in-clinic with the use of instruments but many are specialized tests that can only be run in the lab. The company’s reference labs handle the most complex cases involving immunology, renal, oncology and parasitology related diseases and illnesses. IDEXX’s reference labs service 65k customers/year. Reference lab revenues have grown in-line with the rest of the CAG segment over the past 10 years.

The company’s main growth areas in the CAG segment are instruments (4% of CAG revenues) and the related consumables (35% of CAG revenues). IDEXX sells instruments to veterinary practices and hospitals so that they can provide their clients with detailed diagnostic information about their pets in-clinic, which have much quicker turn-around times than reference lab tests. These are the main classes of instruments that IDEXX sells currently:

Catalyst Dx/One – Chemistry analyzers providing comprehensive diagnostic testing

ProCyte Dx/One – Hematology analyzers providing detailed blood cell analysis

SediVue Dx – Urine sediment analyzers providing advanced bacteria detection

Catalyst analyzers make up about half of the installed base, ProCyte 35% and SediVue 13%. On average, an instrument generates roughly $8.5k-$9k of consumables revenues each year (though it’s implied that Catalyst instruments generate much higher consumable volumes than the average). Consumables have outpaced the growth of the other areas within the CAG segment over the past 10 years. This trend should continue as IDEXX increases the installed base of instruments through its existing line of products and future lines like the inVue Dx Cellular analyzer coming out in late 2024.

The company typically expands the menu of tests that can be run on existing instruments over time so that veterinary practices can continue to get value and effectiveness from their existing instruments. For example, the Catalyst DX instrument which was launched in 2008 has added the ability to test for a dozen or so additional diseases since then. In 2023, consumables revenue from these new tests for the Catalyst instruments accounted for $280M, which is 25% of total consumables revenues.

Because most of the CAG segment revenues are recurring (88% in 2023), organic revenue growth is influenced by certain growth factors. It all starts with vet visit growth. This metric is influenced by pet population growth and the average visits/pet/year. Vet visit growth ranged between +2%-3% each year prior to the pandemic. This coincided nicely with average pet ownership growth of +1%-2% annually. During the pandemic lockdowns, many new pets were adopted at a rate of +6% in 2020 and +4% in 2021 in the U.S. This resulted in visit growth for IDEXX increasing to +3.6% in 2020 and +7.8% in 2021. Most of the growth in visits were from 3Q 2020 to 2Q 2021.

Given that pet adoptions continued to grow at +2% in 2022 and at +1% in 2023, expectations heading into 2022 and 2023 for visit growth were for normalization (i.e. back to +2%-3%). However, IDEXX has experienced declines in visit growth of -2.2% in 2022 and -0.9% in 2023. Some of that was initially explained by the company as veterinary practices adjusting to the staffing shortage and increased cost of hiring. Even with a lot of those macro pressures abating, visit growth hasn’t yet returned.

The more likely explanation for the decline in vet visits could be that a weaker consumer spending environment is resulting in delays, especially on the wellness side, which tends to be a bit more discretionary. The company experienced that impact since the 2nd half of 2023. Another explanation could be that many of the new pet owners from the pandemic years were from a younger cohort of owners, which tend to have less discretionary income.

The next factor is diagnostic testing utilization. Historically, IDEXX has grown diagnostic utilization by 50bps per year, from 13% in 2010 to 19% in 2023. This is broken down into 11% for wellness and 25% for non-wellness visits. Every 50bps increase in diagnostic penetration in the U.S. results in a +1-1.5% boost to CAG recurring revenue growth.

Looking ahead there are a couple of reasons that we can expect this trend to continue. First is that veterinary practices make good money off diagnostics. In 2023, 17% of veterinary practice revenue and 28% of profits came from diagnostics. That’s because diagnostics have the highest margins at 45%. The second reason is that older cohorts of pets tend to require more diagnostics. For puppies and kittens, 1/3 of clinical visits included diagnostics and that number jumped to 50% for senior (7-11 years) and older cohorts. Given that there was a big increase in adoptions in 2020 and 2021, we should see that have a positive impact to diagnostic utilization in the near future.

Pricing is the third factor in determining organic revenue growth. Price increases are set by the company to capture some of the increased value IDEXX is providing its customers and to offset inflation. Historically price increases have ranged between +2%-3% but this ramped up to +5.3% in 2022, +7.8% in 2023 and +5% is expected for 2024. The company argues these increases are justified because veterinary practices set their own pricing for what is charged to the pet owner (usually 2x-3x mark-up). And pet owners on average are still keeping pet spending below 2% of their income (1.6% in 2021). IDEXX also argues that the company delivers more features and functionality each year like DecisionIQ included in VetConnect Plus at no extra cost as an example.

Looking ahead, the expected long-term drivers for CAG recurring revenue growth are +2.5%-4% price realization, +3.5%-4% for increases in diagnostic utilization, +2.5%-3% in installed base expansion and +3% growth in clinical visits. That equates to +11.5%-14% revenue growth for this segment. The company has been below these levels since 2021. To achieve these growth rates, clinical visits have to return to positive growth and utilization needs to improve from current trends. The long-term margin goal is to improve by 50-100bps annually due to 60+% incremental diagnostic margins, lab productivity gains, price increases and increasing software contribution.