AGB 2024.2 - Ashtead Group (AHT.L)

Methodical Share Gains

Subscribe to AGB - One analysis of a good business in each issue.

Ashtead

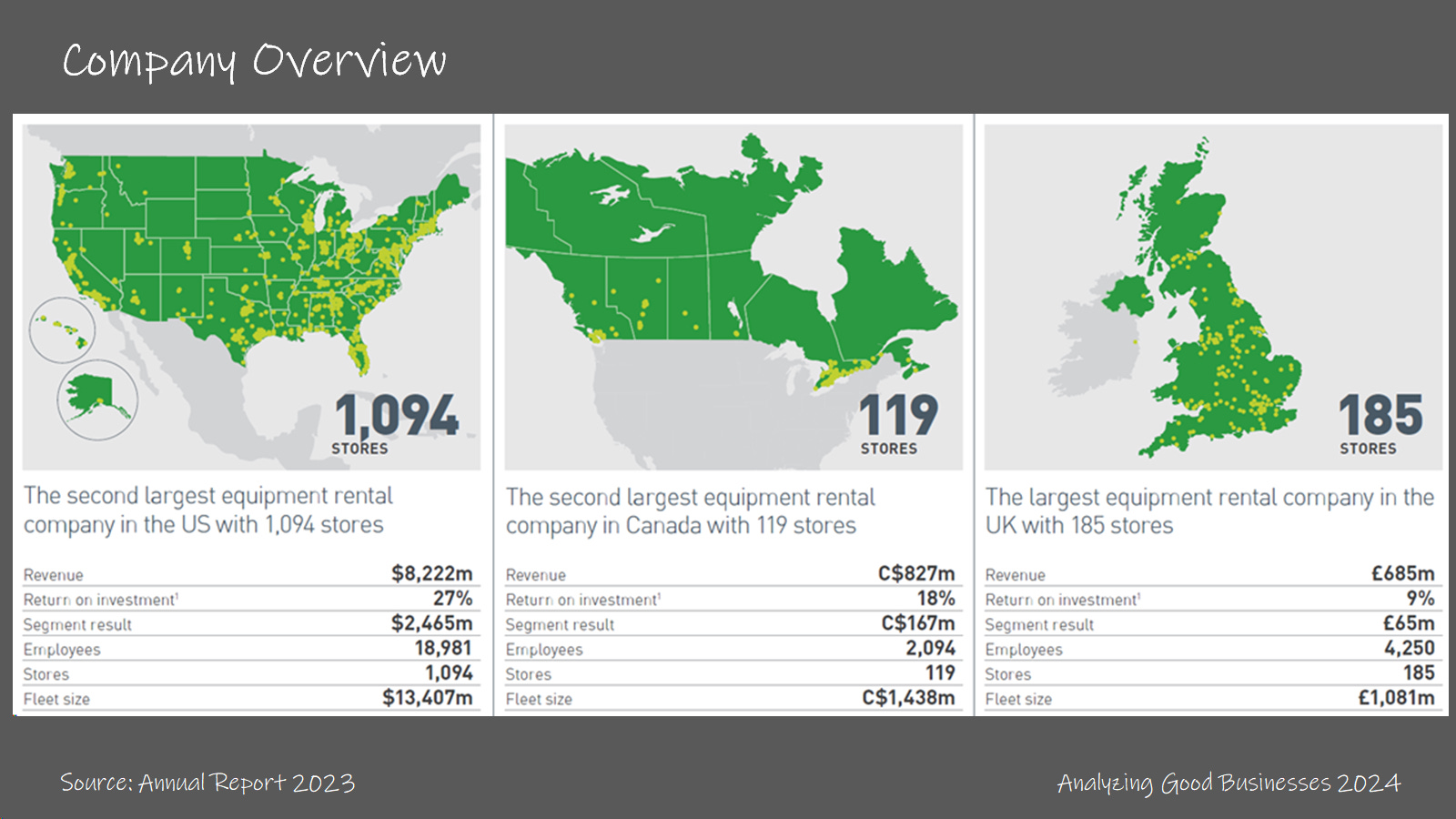

Ashtead is the 2nd largest equipment rental company in North America. The company supports 800k+ customers and has a fleet of 1M+ rental units, which are offered at 1,181 locations in the U.S., 136 in Canada and 191 in the U.K. Ashtead is headquartered in the U.K. but most of the business in the U.S. under the Sunbelt Rentals brand. The company acquired Sunbelt for $2.5M in 1990, which was based in North Carolina. Since then, Ashtead has expanded through a series of bolt-on acquisitions and greenfield location openings. In the U.K. the company has been the leading equipment rental company since 2015.

Customers of Ashtead rent general tools and specialty equipment from the company on demand. Construction end-markets represents 40% of Ashtead’s revenues, of which 90% is non-residential construction. The other 60% is non-construction, of which a large portion is MRO and other specialty equipment. Specialty equipment include power & HVAC, pump solutions, climate control, scaffolding, trench shoring, flooring, etc. and account for ~25% of revenues.

The equipment rental business model is fairly simple. Ashtead purchases general tools and specialty equipment from suppliers and rents it to different customers for a period of time. The company owns assets on average for about 7 years, and then disposes of it in the used equipment market. The annual rental revenues as a % of the initial purchase price is the dollar utilization of the asset. The hypothetical example that the company likes to give is $100 to purchase the asset, $60 in annual rental revenues (implying 60% dollar utilization) and a salvage value of $35. This generates a total of $455 in cash inflows over a 7 year period vs. the $100 initial cash outflow. This doesn’t take into account any costs of maintenance and repairs on the equipment during ownership and the costs to run the service, which would include employee salaries, facility costs, transportation costs, technology costs, etc.

Customers rent from Ashtead and other equipment rental companies because of three main reasons. First, there is flexibility in renting vs. owning. Customers can take on only the cost of renting when there is a need vs. having to own a piece of equipment even when it’s not being utilized. Second, the upfront purchase price is usually large (and going higher with recent inflation) and there aren’t any additional costs involved with renting like repairs and maintenance, storage, asset management, etc. And third is immediate access to the required rental equipment. Customers who buy new equipment typically need to wait 12-18 months to get their orders delivered. Many customers of Ashtead end up selling their owned equipment at the end of its useful life and renting the newer version of it going forward.

Renting has to make sense from a total cost of ownership perspective. Given the high dollar utilization for many pieces of equipment, owning does make financial sense if utilization is moderate to high. That’s why many of Ashtead’s customers both own and rent equipment. Rental penetration is one metric that Ashtead looks at when considering the rental opportunity of a new or existing market. Rental penetration is the percentage of a specific asset available for rent vs. total (owned + available for rent) in a certain market.

For general tools, rental penetration is 55% in the U.S. market. This has increased over the years from 10% in 1990 to 25% in 2000 to 45% in 2011 to today. Drivers of this increase include cost inflation for replacement equipment, more stringent health and safety requirements and better availability of equipment as the rental market has consolidated among larger rental equipment companies. While the rental penetration rate has increased materially over the years, it’s still lower than in the U.K. at 75%. The company has stated that the U.S. rental market could reach well over 60%.

For specialty equipment, the rental penetration rate is much lower at 10% and the company sees an opportunity to close the gap with general tools. While this is a broad average, the rental penetration rates for the different categories of specialty equipment that Ashtead offers is a wide range. Power & HVAC equipment, climate control and flooring are relatively low in 2%-6% range while lighting, ground protection and pump solutions are relatively higher in a 25%-35% range. Ashtead expects that the lower penetrated categories can increase to 15%-20% and the higher penetrated categories can increase to 35%-45% over time.

Growth in specialty has outpaced general tools in recent years. Ashtead’s specialty revenues has grown at double the rate of general tools and reached $2.5B in revenues in fiscal 2023. Just three years prior, in fiscal 2020 specialty revenues were half of that. Some of the outpaced growth in specialty can be attributed to acquisitions. Looking at Ashtead’s largest competitor, United Rentals, we can see similar pattern with specialty outpacing general tools. Specialty revenues for United Rentals accounts for 27% of total revenues, similar to Ashtead’s 25%.

Ashtead’s strategy for growth in specialty is based on clustering many smaller locations (most of which are specialty) around a few large locations in a region. The core idea behind clustering is having a wider assortment of equipment available for customers that need a combination of general tools and specialty equipment to complete a project. This allows Ahtead to be a one stop shop for its customers’ needs in that region.

In 2021, Ashtead introduced its growth plan called Sunbelt 3.0. This initiative had 5 strategic priorities, which were (1) Grow General Tool and Advance Our Clusters, (2) Amplify Specialty, (3) Advance Technology, (4) Lead with ESG, (5) Dynamic Capital Allocation. Most importantly, the goal for Sunbelt 3.0 was to add almost 300 locations in North America, and optimize its operations in the U.K. As the company gets closer to reaching many of its goals for Sunbelt 3.0, the company has telegraphed that it will launch the Sunbelt 4.0 initiative at its Capital Markets day in 2024.