AGB 2023.5 - Brown & Brown (BRO)

Consolidator of Middle Market Insurance Brokers

Subscribe to AGB - One analysis of a good business every five weeks.

Brown & Brown

“We have a unique business, and everybody says that. Everybody's business is unique. I'm just going to tell you Brown & Brown is a very decentralized, very flat management style organization where you actually are compensated individually as a leader or a producer on the results that you drive. So, if you run a business unit or multiple business units, your compensation is tied to the performance of that business unit, whether it'd be in an office, the office, a region, whatever the case may be. And so, we are about growing the business. And we are a business that is an operator of businesses. We are not an acquirer of businesses. We are an operator of businesses that happened to do a lot of acquisitions.” – Chief Executive Officer, J. Powell Brown, at the Barclays Global Financial Services Conferences in September 2013.

Brown & Brown is the 6th largest insurance broker based on 2022 revenues. The company acts as an intermediary between insurance carriers that provide and customers that need insurance products and services. Most of Brown & Brown’s insurance products are under the categories of property & casualty, employee benefits and personal insurance. The company also offers write-your-own flood insurance products through their subsidiary, Wright National Flood Insurance Company, and those products are backed by FEMA, which lowers underwriting risk of this product. Brown & Brown is primarily based in the U.S., with under 7% of revenues coming from international markets in 2022.

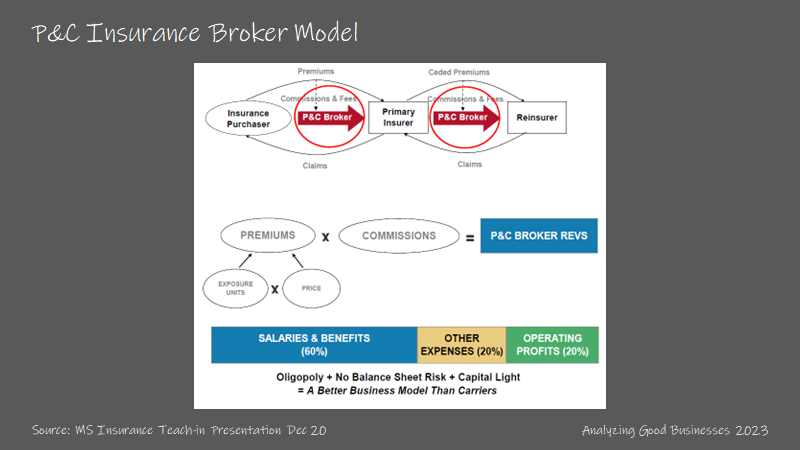

Insurance brokers sit between the supply and demand of the insurance supply chain by facilitating the purchase of insurance products as well as managing records and providing services. Carriers underwrite the risk of insurance while collecting a premium and seek the help of insurance brokers to find customers (usually commercial) to purchase their products. Brokers will work with many carrier partners to find the right insurance product (and price) for its customers. Brokers source new customers through their agents who sell to the business communities in those regions. Brokers typically don’t assume any underwriting risk and require little capital to run their businesses.

Brokers earn a commission for a successful sale, typically in the range of 10%-15% of the annual premiums placed. The commissions for personal lines of insurance are on average lower than commercial lines due to the increased complexity to commercial insurance. The drivers of revenues for insurance brokers are (1) fluctuations in “exposure units”, which can be thought of as the amount of dollars of value under coverage, and (2) changes in premium rates (prices). Exposure units can be impacted by the number of customers, the number of insured units by each customer, and changes in the values of the insured units. For Brown & Brown, the company states that growth is impacted 1/3 to 1/4 by changes in price and the remaining 2/3 to 3/4 by changes in exposure units. Brokers also earn fees, which are related to services that include third-party claims administration.

Pricing is an interesting dynamic for the insurance brokerage industry. Premiums for insurance products fluctuate, depending on supply and demand for insurance coverage. Let’s use a natural disaster as an example. After a flood or hurricane, there will be large losses by the carriers, with the magnitude depending on how disciplined the underwriting standards were. This will likely result in fewer carriers electing to cover that risk in the future, leading to reduced supply. Carriers that elect to remain in that market will raise prices to make up for the large losses and the reduced supply. On the demand side, more customers will try to gain coverage, even if they weren’t affected. And that supply demand imbalance creates a hard market. Insurance brokers typically benefit during a hard market because their commissions are based on a percentage of the premiums, leading to increased organic revenue growth.

The insurance brokerage industry has been undergoing a wave of consolidation for the past two decades. While the industry is still fragmented, the larger brokers have been acquiring many of its smaller competitors, usually at reasonable valuations. Because the industry experiences organic revenue growth between 0%-5% in normal markets and much higher than that in hard markets, these acquisitions are sustainable and self-funded. Aside from brokerage firms, banks also competed for acquisitions in the early 2000s. That shifted to private equity firms since the great financial crisis of 2008. Brown & Brown has stated that there over 30 private equity firms active in the space.

Brown & Brown is one of many insurance brokers, but there are some unique characteristics worth mentioning. First, the company operates under a decentralized model, where local branding isn’t necessarily under the Brown & Brown umbrella. This is especially true if Brown & Brown has acquired an established insurance brokerage firm in a region. Typically, the acquired company keeps its branding and Brown & Brown handles the back office and other needs. Each branch is responsible for their own P&L and most costs are allocated at the operating level. The company has stated that corporate overhead is 5.5% of revenue vs. 9%-18% for the industry.

Second, the company is still family run, even after 84 years of existence. Current CEO, J. Powell Brown has been CEO since 2009, succeeding his father J. Hyatt Brown, who is now chairman of the board. J. Hyatt Brown was the CEO for 48 years. The family owns 16% of the company, and the Brown & Brown employees own another 5%-6%. At least 60% of employees own stock in the company.

Third, the company mostly competes in the middle market (businesses wuth 20-1000 employees), which means dealing with fewer large customers and less competition from larger brokers. This ties in with the company’s decentralized model and branding. The middle-market represents 10%-15% of the firms in the U.S.

Brown & Brown segments their business into four buckets: Retail, National Programs, Wholesale Brokerage and Services.

Retail is the largest segment at 58% of revenues in 2022. This segment is the traditional outbound sales of insurance. Brown & Brown agents will meet with customers (usually commercial) a plan to purchase insurance coverage based on their needs. This segment has slightly below (1%-2%) EBITDAC margins at 31.9% vs. the company average of 33.2%.

National Programs represent 24% of revenues. This segment has increased as a percentage of revenues since over the past 20 years. National Programs are specialized insurance programs for niche markets (certain industries, trade groups and professions). The insurance carriers that support these products oftentimes give Brown & Brown authority to handle underwriting and claims administration for these programs. There are 40 programs that are offered, partnering with over 100 carriers. Catastrophic insurance programs are under this segment. National Programs has the highest EBITDAC margins at 40.1%.

Wholesale Brokerage represents 13% of revenues. This segment sells surplus commercial and personal lines of insurance to customers through a network of brokers. Typically agents of smaller brokerages that don’t have access to certain insurance products will utilize Brown & Brown’s wholesale offering. This segment has similar margins to Retail at 31.1%.

Services is the smallest segment at 5% of revenues. Fees are generated when Brown & Brown assists clients with claims administration and other services to policy holders. This segment has the lowest EBITDAC margins at 19.1% but is higher than others in the industry.

The company’s margins are the highest among the large publicly traded peers. Brown & Brown’s lean cost structure does help with its margin advantage but also its large exposure to National Programs, which tend to have EBITDAC margins in the range of 37%-40%, due to its lower employee costs in the segment. Brown & Brown targets EBITDAC margins of 30%-35%, and the company has been in the 30%-33% over the past 7 years.