AGB 2023.10 - Equity Lifestyle Properties (ELS)

Consistent Rate Increases

Subscribe to AGB - One analysis of a good business every five weeks.

Equity Lifestyle Properties

Equity Lifestyle is one of the two largest owners of manufactured housing (MH), recreational vehicle (RV), marina properties. As of the third quarter of 2023, the company owns and operates 72.7k MH sites, 62.7k RV sites and 6.9k Marina slips across 450 properties in 35 U.S. states and Canada. Many of the properties are located near retirement and vacation destinations, of which many are near lake, river and coastal areas. Equity Lifestyle was founded in 1984 by real estate investor, Sam Zell.

The company operates a relatively straight forward business model. Customers rent sites at Equity Lifestyle owned properties under annual or monthly terms. Most leases are annual and usually have rate changes during renewal. There are certain properties that are under longer-term leases and most of these are also subject to annual rate changes. In exchange for the rental fee, customers get access to live on the site, either in a MH, RV or dock their boats in a marina. Customers also get access to the common area facilities and amenities, which sometimes includes a clubhouse, swimming pool, laundry facilities, golf courses, tennis courts, exercise rooms, etc.

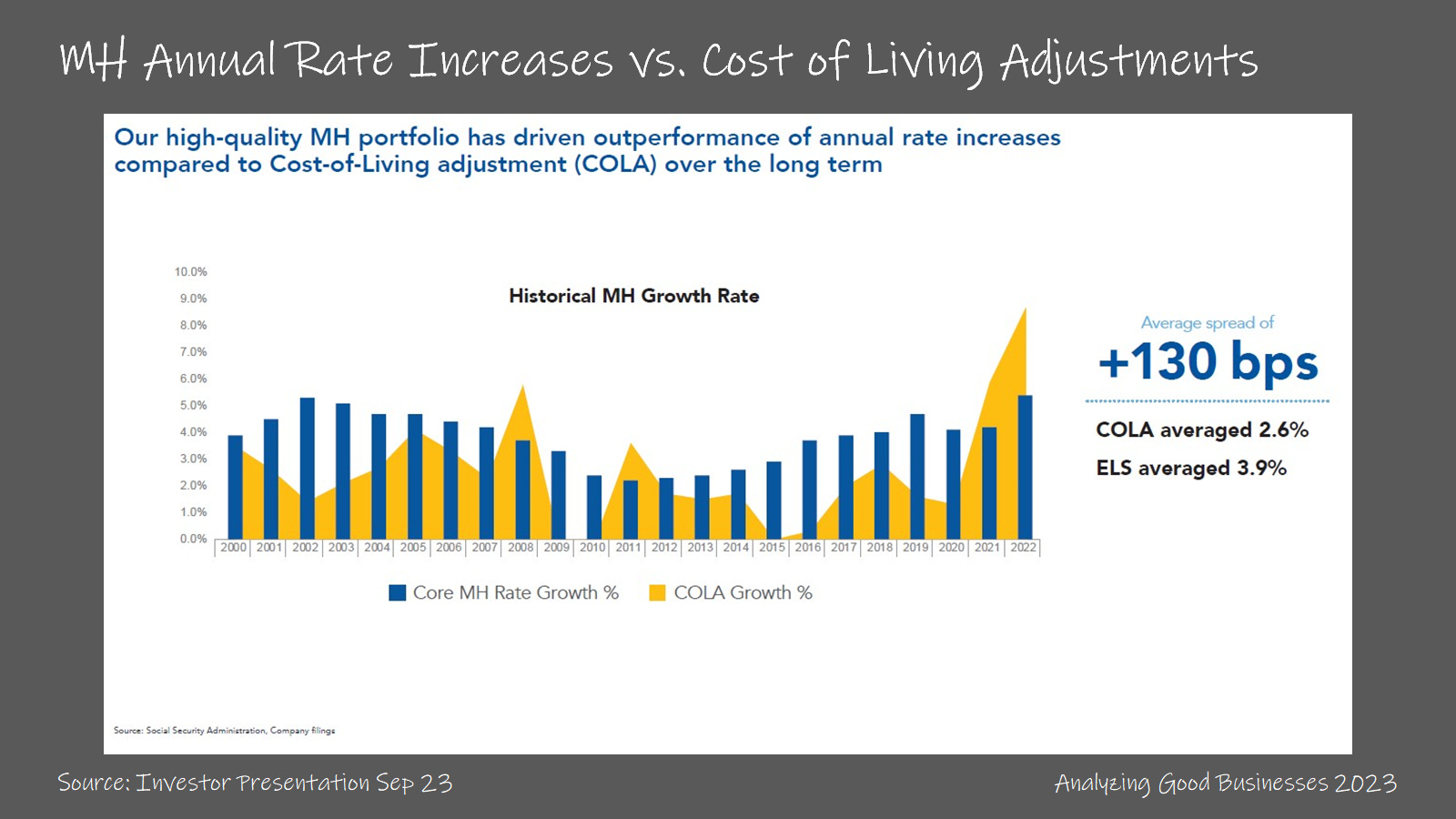

The MH segment represents over 51% of total available sites and annual MH revenues are over 60% of property operating revenues. Since 2000, annual rate increases in the MH portfolio have averaged +3.9%. This is higher than the Cost of Living Adjustment growth calculated by the Social Security Administration, which averaged +2.6%. Specifically for the MH segment, a quarter of the company’s leases are linked to CPI growth, of which half (or 12.5%) are directly linked to CPI and the other half have price increase floors of 3%. Rates for the remaining 75% are market driven. These rate changes are generally accepted by most of Equity Lifestyle’s customers, given the low annual turnover rate. In certain states like Florida, rate increases are negotiated between the company and representatives of the home owners association.

Typical MH customers of Equity Lifestyle are older (new home buyers are near 60 years old) with good credit scores (700+ FICO). Customers are looking for a second home near a vacation destination, which is more affordable than a typical single family home. Most customers purchase the MH outright without a mortgage. Many use part of the equity in their primary residence to fund the MH purchase. And while this is a large sum of cash and is more than a typical down payment on an average single family home, the monthly cost is much lower because there is no mortgage payment. MH owners only pay the rental rate to gain access the site and community amenities.

In 2023, the average upfront cost for a MH was $127k with a monthly cost of $797. Comparatively, an average single family home had an upfront cost of $106k (20% down payment on a $528k home) but came with a monthly cost of $2.6k. On a per square foot basis, MH owners pay less in the range of 25%-30%. A small minority (just 2% over the past 3 years) finance their purchase with Equity Lifestyle. This is partially due to the stringent mortgage regulations and higher cost of debt for homes on land that is leased from another party.

Most of the company’s MH customers own their home, with just 4% renting in 2022. Renters made up a larger portion of the Equity Lifestyle’s customer base in the past at 9% in 2013. The percentage of renters has since trended lower each year. That’s also reflective of a stronger economy so that trend could reverse in a downturn. The company views its rental program as a try “before you buy” option for its customers. These conversions are meaningful. In 2019, 33% of total MH sales were the result of a renter conversion.

The RV and Marina segment represents 49% of total available sites and RV and marina revenues are 32% of property operating revenues. RV customers can choose annual, seasonal (up to 6 months) or transient memberships. Annual customers pay a lower effective daily but pay for the full year. Annual RV rents are close to $500/month and transient rents are ~2x that amount. Revenues from seasonal and transient customers are higher in the first and third quarters of the year.

Equity Lifestyle seeks to convert transient RV customers to seasonal and then eventually to annual. While the effective daily rate for annual memberships are lower than seasonal or transient, the occupancy rates are much higher. Based on Sun Communities’ data, occupancy rates for transient are 1/3 that of annual, and a successful conversion to annual results in a 40%-60% increase in revenues after the first year. Furthermore, there are fewer marketing costs necessary to retain an annual customer. For Equity Lifestyle, transient RV revenues are ~7% of total RV revenues. The company has averaged 20%-30% conversion rates each year and has decreased the number of available transient sites.

Occupancy is decent measure of the collective health of the company’s customer base. Equity Lifestyle had steadily increased its “same store” occupancy rate from the great recession up to 2019. Since then, the occupancy rate has ranged between 94.9%-95.3%. Things that impact overall occupancy include the percentage of sites that are annual vs. seasonal/transient and how much exposure the company has in MH vs. RV. Ground up builds and expansions also have an impact on occupancy because these take much longer to fill vacancies than if the company had acquired an existing property. Within the MH portfolio, the company states that occupancy for more than half of its communities are over 98%, so there is still more room for improvement.

The markets for MH and RV properties are fragmented with Equity Lifestyle and Sun Communities each commanding less than 10% of these markets. The top 10 command close to 30% of these markets. The marina market is even more fragmented with Equity Lifestyle and Sun Communities commanding less than 10% combined. Fragmentation implies there is still more room for acquisition led growth, especially since new builds are harder to construct near highly valued vacation destinations.

Most of the company’s property growth in recent years has been in the RVs and marina segments. Since 2017 when the company first disclosed its acquisitions by segment type, MH sites have accounted for just 16% of total acquisitions. RVs were 58% and marinas 26%. In terms of total number of sites, the company has increased MH sites from 2013 to 2022 by 2.8k or 4%, while RVs increased by 20.2k or 48%.