AGB 2023.1 - Vulcan Materials (VMC)

Benefiting from Infrastructure Tailwinds

Subscribe to AGB - One analysis of a good business every five weeks.

Vulcan Materials

Vulcan Materials is the leading producer of aggregates in the U.S. with ~10% market share in 2021. The company has the #1 or #2 position in ~90% of its markets and its facilities are strategically located in 35 of the top 50 MSAs in the U.S. across 22 states. Vulcan also provides asphalt and ready-mix concrete in certain states, which are vertically integrated with its aggregates production facilities. The company has over 22k customers.

Aggregates are primarily crushed stone, sand and gravel, usually sourced from a local quarry. Once mined, the stones are crushed and separated into various sizes for different use cases. Aggregates are a key material used for the construction of highways, parking lots, bridges, schools, commercial and residential buildings and other key infrastructure. As an example, a typical interstate highway requires 21 inches of aggregates laid on compacted soil and another 11 inches of concrete on top.

Priced between $10-$15/ton, aggregates have one of the lowest ratios of value to weight among construction materials, making proximity to the end customer very important from a cost perspective. Over 60% of the U.S. population lives 60 miles from a Vulcan owned aggregates facility. The end products are delivered to customers by trucks, trains and ships, with over 80% of the transportation being done by truck. Trucks have carrying capacity of 20-25 tons. Train cars can hold 4-5 truckloads and ships can hold 65 truckloads.

Customers of aggregates can be broken down into publicly and privately funded construction. In 2021, 42% Vulcan’s aggregate revenues were for publicly funded construction, of which 22% were for highway construction. The remaining 58% were for privately funded construction. Non-residential construction makes up the most of aggregates volume accounting for ~40%. Residential constructions makes up ~22%, highways ~23% and other non-building infrastructure ~15%.

As a general rule, non-residential construction and public infrastructure are more aggregates intensive than residential construction. According to Morgan Stanley, ~38k tons of aggregates are required for the construction of one mile of a four lane interstate highway. By comparison, the average home requires ~400 tons of aggregates and the average school or hospital requires ~15k tons, mainly for the support and foundation of these buildings.

Publicly funded construction is typically less cyclical than privately funded construction because public sector spending on infrastructure is supported by Federal funding bills. From 1998-2005, it was the Transportation Equity Act for the 21st Century (TEA-21); from 2005-2012 it was the Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users’ (SAFETEA-LU); from 2012-2015 it was the Moving Ahead for Progress in the 21st Century (MAP 21); and from 2015-2021 it was the Fixing America’s Surface Transportation (FAST) Act. The states in which Vulcan has a presence benefited from these funding bills more than other states, except during SAFETEA-LU era.

In 2021, the Infrastructure Investment and Jobs Act (IIJA) was signed into law. The bill was for $1.2T, of which the Federal Highway Program funding was the largest part. This program starts at $66.9B in 2022 and increases to $72.1B in 2026 for a total of $347.5B over the 5 year time period. This is the largest increase in federal highway, road and bridge funding in many decades.

Privately funded construction is more cyclical as many projects are correlated with job growth and demographic trends. Growth in the workforce creates demand for housing as well as offices, shopping centers, warehouses, restaurants, etc. A slowdown in the economy does have an impact on aggregates demand. From a profitability stand point, there isn’t much difference for Vulcan to sell aggregates to publicly funded or privately funded construction customers.

The company’s aggregates segment contributed 72% of revenues and 94% of gross margin in 2021. Vulcan also has an asphalt segment, which makes up 14% of revenues and 2% of gross margin. Asphalt is considered a downstream business from aggregates because aggregates is a key input to make asphalt and makes up 95% the weight. Aggregates are mixed with liquid asphalt cement, which the company purchases from third parties, to make asphalt. Vulcan sells asphalt in a few states like Alabama, Arizona, California, New Mexico, Tennessee and Texas. Margins are much lower in asphalt (3% vs. 30% for aggregates) because the extra cost of liquid asphalt cement and the fact that asphalt is very temperature sensitive. Asphalt has a higher mix of privately vs. publicly funded construction demand.

Vulcan’s concrete segment makes up 14% of revenues and 4% of gross margin. This was lower in the past but the company acquired U.S. Cement in 2021, increasing its contribution mix from concrete. The company sells ready-mix concrete in a few states like California, Maryland, New Jersey, New York, Oklahoma, Pennsylvania, Texas, Virginia, the U.S. Virgin Islands, and Washington D.C. Aggregates make up 80% of the weight of concrete. Because ready-mix concrete hardens quickly, usually the end customer has to be in close proximity to the production facility. This segment also has lower margins at 7% because of the extra input costs required and the lower barriers to entry in producing this product.

The aggregates industry is very fragmented with over 5.5k companies and 11k operations. The company estimates that 2/3 of the industry is owned by small regional players, implying that consolidation is still an ongoing trend. The top ten producers commanded 15% of the market in 1983, reached 21% by 1992 and now command 33%. Vulcan is the leader at ~10% and Martin Marietta Materials is a close second.

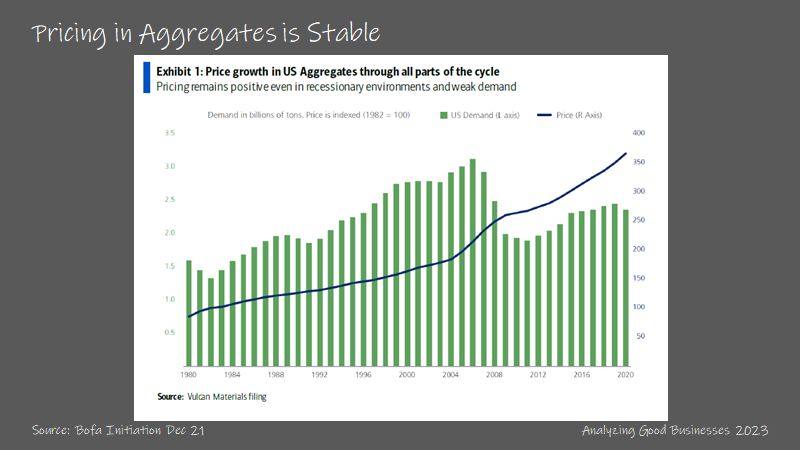

Prices of aggregates, unlike other construction materials, tends to trend upwards even during periods of slowing to negative demand. Reasons for this dynamic are (1) aggregates are essential for construction but have almost no substitutes, (2) aggregates have low value/weight, meaning they can only be economically sourced by the end customer from local facilities, (3) aggregates are a small portion of the total cost of a project (2%-10% range), and (4) quarries can start and stop operations with ease (15 minutes to shut the operation down). This results in annual price increases that are almost always positive. Even during drop in demand during and after the Great Recession, prices remained flat or positive. Industry average prices have increased at a CAGR of +4.3% from 2003-2020 and Vulcan did better at a +5% CAGR during the same period.

Financial metrics that are important to the company are gross profit/ton and incremental margins. At Vulcan’s 2019 Analyst Day, the company provided a target of $9 in cash gross profit/ton on 230M-240M tons of volume, which implies $2B in EBITDA. The company reached $7.43 in cash gross profit/ton in 2022 and volumes of 223M tons. At the 2022 Analyst Day, the company provided a new long-term target of $11-$12 in cash gross profit/ton on volumes of 260M-270M tons, resulting in an EBITDA target of $2.7B-$3B. As for incremental margins, the company aims for 60% flow through on a gross profit/ton basis.