AGB 2022.5 - SiteOne Landscape Supply (SITE)

AGB 2022.5 - SiteOne Landscape Supply (SITE)

Consolidating Distributor in a Fragmented Value Chain

Subscribe to AGB - One analysis of a good business every three weeks.

SiteOne Landscape Supply

There are many similarities between SiteOne and Pool Corp (you can read our write-up here). Both are leading B2B distributors of products for outdoor spaces and connect many different suppliers to professional customers. Even the company’s management thinks of SiteOne as Pool Corp 15-20 years ago, implying that there is still ample runway for consolidation + growth in the industry. After doing the research, we think the key differences between the two companies are (1) SiteOne’s product lines are more diverse, which should result in lower LT margins than Pool Corp, (2) the supplier base is more fragmented in landscape supplies, (3) and SiteOne is much more acquisitive, resulting in a higher reinvestment rate.

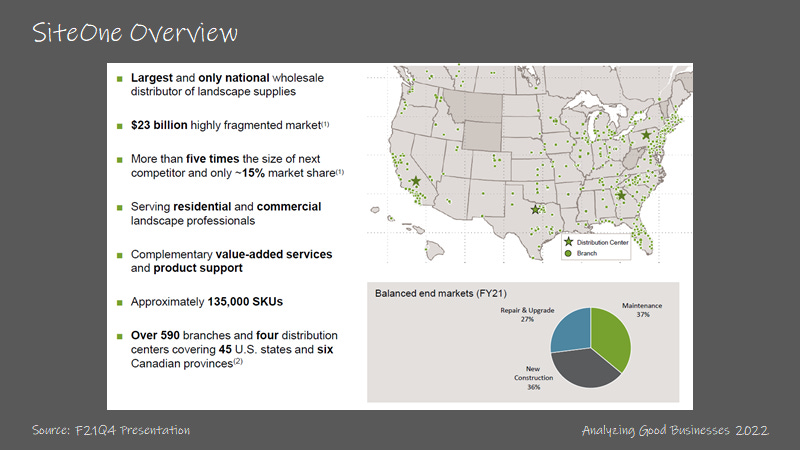

SiteOne is the leading wholesale distributor of landscape supplies in the U.S. The company primarily sells its products through its 590 branch locations in over 45 states and 6 Canadian provinces, which are supported by SiteOne’s 4 distribution centers. Branch locations range in size between 5k to 15k square feet and oftentimes have outside storage yards between 10k to 20k square feet if they offer nursery and hardscape products.

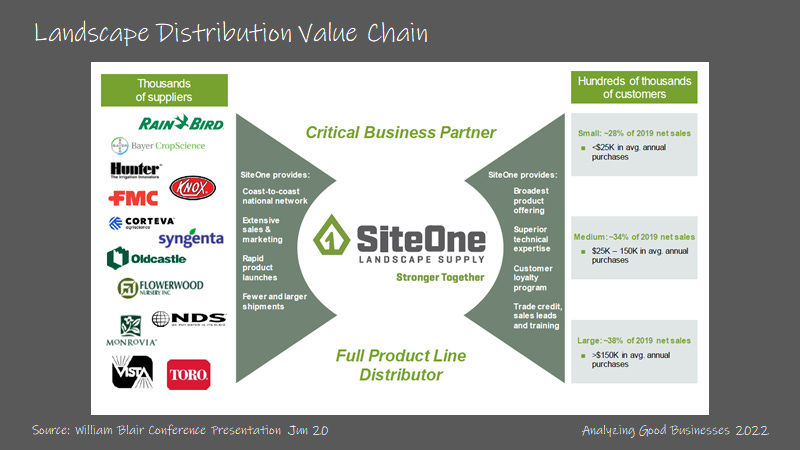

The $23B market for landscape distribution is fragmented in all parts of the value chain. SiteOne has relationships with over 5k suppliers, which provide 135k SKUs that the company sells to 280k customers. Due to the large number of product categories for landscaping services, distribution for landscape supplies is more fragmented than pool supplies. SiteOne’s top three suppliers account for less than 20% of COGS, while Pool Corp’s top three make up almost 40%.

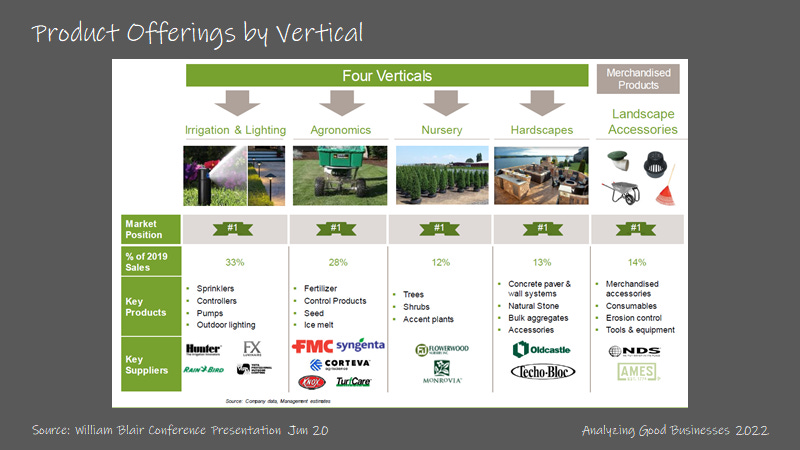

SiteOne categorizes its product lines into irrigation (30% of 2021 revenues), agronomics (26%), nursery (10%), hardscapes (13%) and accessories (21%). And while the company provides 135k different SKUs, not all of these items are available in each branch location due to the availability of outdoor space. The company is working to increase the number of locations that have full product availability (currently ~21%).

On the customer side, there are hundreds of thousands of residential and commercial landscape professionals that provide design, installation, repair and maintenance services of outdoor spaces. SiteOne has over 280k customers in their database, of which 43% are large (>$150k in spending), 33% medium ($25k-$150k) and 24% small sized (<$25k) customers. Many customers buy supplies on an as needed basis for maintenance work (especially the smaller ones). And for installation projects, customers often require only small quantities of products from many different suppliers for each job, making it necessary to purchase supplies through a distributor like SiteOne.

As the largest national distributor, SiteOne does skew more towards larger customers. This makes sense as the company is better positioned to win national and regional accounts due to its footprint. Some of SiteOne’s largest customers even have direct distribution agreements in place, taking advantage of the company’s supplier relationships. In these cases, SiteOne doesn’t take on the inventory and the products are directly distributed to the customers’ sites. Typically, landscape supplies only account for 10% of the total cost for maintenance and 25% for large commercial installation jobs. Labor is usually the largest cost, which implies product selection, availability and supply chain efficiency are much more important.

SiteOne commands over 15% overall market share, which is 5x the size of the #2 player. The market share differential between SiteOne and the rest of the market has increased since coming public in 2016. A lot of that has to do with the pace at which the company is making acquisitions each year. Since 2015, SiteOne has added almost a billion dollars in revenue from 56 acquisitions. Distribution of landscape supplies is also very fragmented. SiteOne estimates that there are over 1,000 distributors in the U.S.

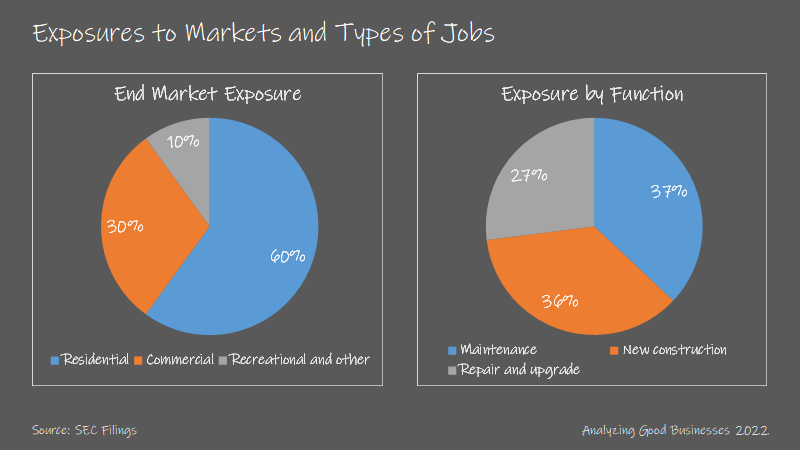

Similar to distribution of pool supplies, growth in landscape distribution is directly and indirectly driven by new construction and housing turnover. Construction contributed to 36% of SiteOne’s revenue in 2021 and repair/remodels contributed 27%. Maintenance was 37% of revenues, but is typically higher in the low 40s%. Compare that to pool supplies distribution, which is 15% new construction, 25% R&R and 60% maintenance. For new construction, landscaping installation usually begins 6 months after the start, similar to pool installations.

After the company’s IPO in 2016, margin improvement initiatives were put into place. These included pricing optimization initiatives, category management (reorganizing products around a preferred set of suppliers), more emphasis on private label, better inventory management (barcoding was introduced) and the build out of three distribution centers in 2017. Through these efforts and topline growth, EBITDA margins expanded from 6.7% in 2016 to 11.4% in 2021. LT margins are following a similar trajectory to Pool Corp’s but management believes that there is a structural challenge because landscape supply is more complex. There are more products to supply to customers and products in the nursery and hardscape categories are more costly to serve.

Why is it a good business?

For new construction landscaping projects or repair/remodel jobs, these service are for the most part done by professionals. And because the supplies required for each project are different and there is fragmentation on the supply side, it makes sense that distributors are the main source for landscaping supplies (home improvement stores like Home Depot and Lowe’s account for 9% of the industry). For maintenance work, a meaningful percentage of residential homeowners may do it themselves, but most homeowners that have had a repair/remodel job done by a professional are more likely to hire someone else for maintenance.

In analyzing the outdoor spaces landscaping market, there is no relevant data on installed base or aging stock of outdoor spaces. (Whereas in analyzing Pool Corp, one can point to the average age and the number of installed underground pools). Each outdoor space is different, depending on the size of the space and whether it’s a residential or commercial job. Furthermore, these outdoor spaces don’t age at a similar trajectory like an underground pool does.

As the largest distributor of landscape supplies, SiteOne benefits from scale advantages, which mainly are (1) sourcing, (2) private label, (3) more efficient distribution which benefits both Site One and the customer. As the company has increased in size, SiteOne has been able to increase the number of SKUs that it supplies (100k in 2016 to 135k in 2021). Part of that has to do with filling out some product categories within nursery and hardscapes through acquisitions. The company also has a strong position when negotiating purchase orders. And because there are generally volume based incentives from suppliers, SiteOne can source products cheaper.

Private Label is another area where SiteOne has been able to grow with size. LESCO is the company’s largest private label brand in the agronomics segment and is the 4th largest recognized brand in the market. SiteOne Pro-Trade was recently introduced, which are professional grade lighting fixtures and tools. Private label currently represents 15% of revenues and the company has stated that the goal is to get private label to 30% of revenues.

In 2017, SiteOne opened the first three large scale distribution centers in Georgia, California and Pennsylvania. A lot of the working capital investment in 2017 was related to these openings. Smaller packaged products products go through distribution centers (mainly irrigation, chemical, tools and accessories) and the larger/bulkier products like fertilizer, hardscapes, and nursery products still go direct to store.

The main benefits are increased efficiency in the fleet and better product availability for customers (and reduced delivery times to customer job sites). Prior to the buildout of the distribution centers, over 2/3 of products were nationally sourced and delivered to all 590 branch locations. This meant more trips to the branch locations with less than full truck loads. The company recognizes that there is an opportunity to increase inventory turns from the high 3x/low 4x to over 5.5x. SiteOne estimates that a half turn of improvement would result in $15M-$20M in additional free cash flow. It’s easier said than done though. Pool Corp has maintained inventory turns in the high 3x range over the past decade.

On the acquisition side, scale helps the company as it is the natural buyer for many smaller distributors. For many years, SiteOne has stated that over 90% of deals are exclusively negotiated (this number was 95% in 2019), which means that the company can usually purchase these assets at very attractive valuation multiples.

Returns on incremental capital?

Over the past 8 years, SiteOne has spent 13% of its capital on capex and 87% on acquisitions. By comparison, Pool Corp is closer to 45%/55%. Most of the capex spend is related to the buildout and maintenance of branch locations, the company’s fleet and the distribution centers. The company has also invested in its eCommerce capabilities, which was fully revamped in the beginning of 2018. Customers can order products online and pick them up in store or have them delivered to the job site. eCommerce orders allows the store employees to be more efficient as it increases store utilization with fewer bottlenecks at check out.

While the company is still building out greenfield branch locations, SiteOne’s view is that the time and effort it takes to ramp a new location up to full productivity make acquisitions a better use of capital. SiteOne aims to acquire leading distributors, so the company gets an experienced team and the relationships with the local customer base.

It also seems like there are enough distributors in key locations to acquire (as opposed to needing to build greenfield branches) as the barriers to entry in this business are relatively low. Goldman estimates that the cost of opening a landscape distribution location is only $50k-$60k. There are other costs that go with that, including a sales team and delivery infrastructure.

Because most acquisitions are negotiated exclusively (17 of 18 deals in 2016/2017 were exclusive), the valuation multiples paid are low, resulting in high returns on capital. Since 2014, SiteOne has been able to acquire targets in aggregate at 0.65x trailing revenues. And SiteOne has stated that deal multiples are less than 7x EBITDA before synergies. Assuming that deals are roughly 5x-6x EBITDA post synergies, it would imply that the pre-tax return on acquisitions is close to 17%-20%. This is before any subsequent growth of the acquired assets.

We estimate that SiteOne has generated returns on incremental capital between 20%-30% in the past 4 years. Due to the heavy working capital investment into the distribution centers in 2017, the return calculations for that year are a bit skewed negatively. Interestingly there wasn’t a massive jump in the returns in 2021 like we’ve seen with Pool Corp, but that’s partially due to the inventory stocking that the company did to get ahead of any potential supply chain disruptions and the buildout of its 4th data center in Texas.

Reinvestment potential?

For 2021, the landscape supply distribution market was $23B, and that number has grown by +6.3% CAGR since 2016. Nursery makes up 1/3 of the industry, accessories at 1/5, and other categories like hardscapes, control products, irrigation, fertilizer and lighting make up 1/10 each.

By comparison, SiteOne has grown its top line by a +16% CAGR since 2016, increasing both the number of branch locations and the revenue/branch location. As mentioned previously, Site One commands 15% market share, which is higher than the 9% share at the time of its IPO in 2016. The other players don’t have national scale just yet. #2 is Ewing, which is focused on irrigation and 1/5 the size of SiteOne. #3 is Horizon, which is owned by Pool Corp.

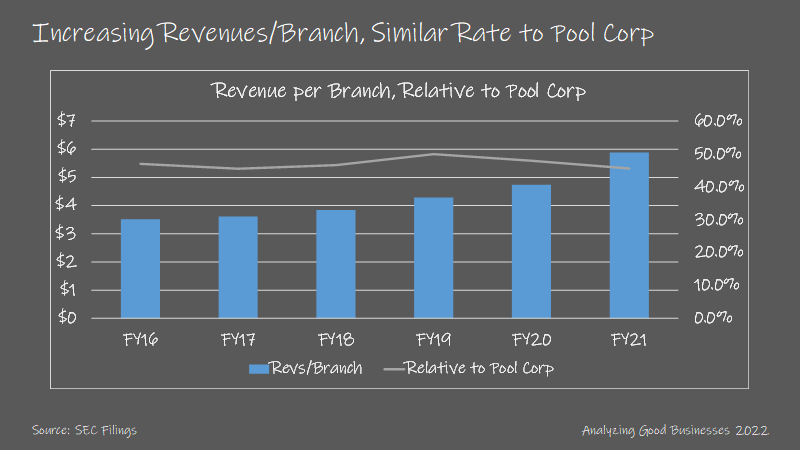

If we compare SiteOne to Pool Corp by branch location (understanding that there are differences in the size and business model for these two companies), SiteOne’s revenues/branch has consistently remained at 45%-50% of Pool Corp’s. It will be interesting to see if the company can close that gap as it increases its market share.

We also have to keep in mind that the revenue/branch calculation for Pool Corp is for the whole company (blue + green businesses), so it’s likely that the pool supplies branches have even higher metrics. SiteOne has stated that the SG&A levels for landscape distribution are structurally higher than pool supply distribution due to the bulkiness of some of the products as well as the higher number of SKUs.

On the acquisition front, the company estimates that there are 1k distributors of landscape supplies in the U.S. and 25% of these are worth acquiring. SiteOne has branches in half of the 384 MSAs in the U.S., so future acquisitions will likely increase SiteOne’s coverage of new markets over time.

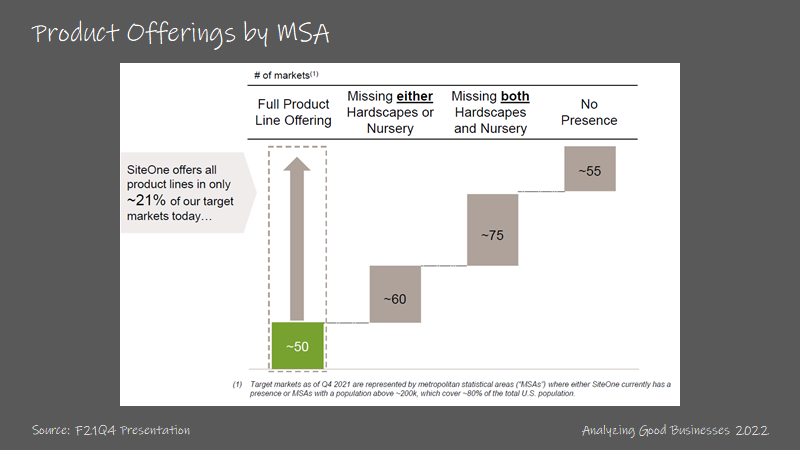

The company also can invest in offering its complete line of products in more markets. SiteOne only offers its full product line in 21% of its target markets and is missing either hardscapes or nursey in most of the locations without the full product line offering. The company has mentioned that branch locations with the full product line are more profitable because customers can get most of their supply needs from one single location.

SiteOne is also under-indexed to smaller customers. When the company was at 13% market share in 2020, SiteOne mentioned that the company’s share of larger customers was 20%-25% but only 6%-8% of smaller customers. One way for the company to gain more mindshare with smaller customers would be to make a better effort to enroll more of the smaller customers into their Partners Program. Currently roughly 50% of revenues are account from members of the program, a number that has remained relatively stagnant since 2016.

With a reinvestment rate between 65%-75% and a return on capital between 20%-30%, we estimate that SiteOne has increased its intrinsic value between 15%-20% over the past 4 years. Compared to Pool Corp’s reinvestment rate of 20%-25%, SiteOne has put back more of its capital back into the business. It makes sense as SiteOne is in the earlier stages of its company life cycle and it has many more opportunities to consolidate the market.

What else is important?

Over earning during Covid

Similar to other companies that are exposed to housing, SiteOne benefitted from the increased demand from new and existing homeowners during Covid lockdowns. Revenue growth accelerated to +14.7% in 2022 and +28.5% in 2021. This is similar to (but not as high as) Pool Corp’s +23% and +34.5% growth, respectively.

There wasn’t as much of a spike for demand of maintenance products like there was for pool supply. And SiteOne was actually good about limiting supply disruptions in 2021 by making large advanced inventory purchases, which coincided with the build out of the company’s new distribution center in Dallas, Texas. We should see some of the working capital investment roll off in 2022.

When housing does start to rollover, it’s also worth keeping in mind that maintenance products are 40% of SiteOne’s revenues (vs. 60% for Pool Corp).

Competition from Pool Corp

Pool Corp owns the #3 player in the industry, Horizon, and continues to invest in its growth. Horizon currently has coverage in the southern and western states but the company is investing for growth. Pool Corp also has the benefit of integrating Horizon with the back-end technology and distribution capabilities of the Pool Corp’s blue business. This may allow Horizon to benefit from many of the same scale advantages even before reaching the size of SiteOne.

Judging from the recent past, SiteOne’s superior acquisition engine should allow the company to stay ahead of Pool Corp in the number of branches in landscape supply in the near-term. But competition from Pool Corp, especially on the acquisition side is something to be mindful of.

Optionality

Because the consolidation opportunity is so attractive right now, the company doesn’t really need optionality. Geographic expansion would be a way to increase the TAM, but the company already has a presence in Canada.

SiteOne should do more with private label, given its market share vs. the competition. Private label products generally command much higher gross margins and this could help bridge the gap between SiteOne’s and Pool Corp’s margins. Pool Corp’s private label products represent ~25% of revenues, higher than SiteOne’s 15%. The company has stated that the 30% is the goal for private label, but it has remained closer to 15% for many years.

If you made it this far, I hope you received some value from reading our analysis. Please subscribe to the newsletter and share with anyone that would find it valuable. Thank you for your support!

How do periods of high inflation impact their margins? Pretty meaningful bump in margins from 2019 --> 2022