AGB 2021.9 - Constellation Brands (STZ)

Highly Prized Mexican Beer Business

Subscribe to AGB - One analysis of a good business every two weeks.

Constellation Brands

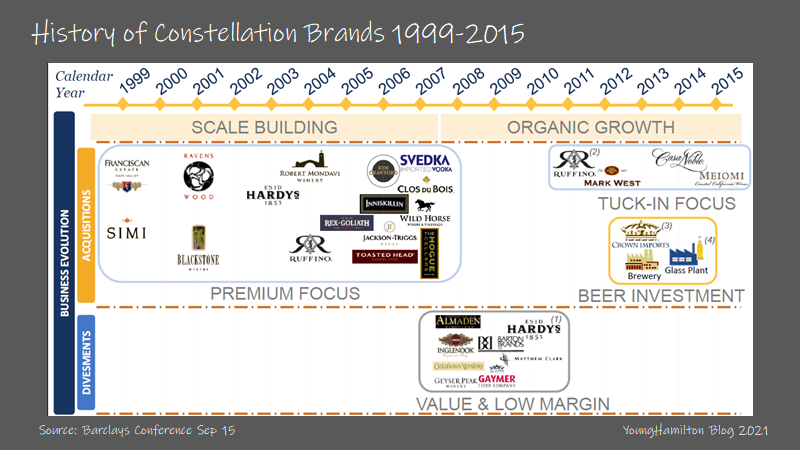

Constellation Brands is the leading producer of imported beer to the U.S. under the Corona, Modelo and Pacifico brands and is a leading producer of wines (Robert Mondavi, Kim Crawford, Meiomi) and spirits (SVEDKA, Casa Noble) globally. The company has a long history of acquiring and divesting brands in the beer, wine and spirits categories, building scale and distribution expertise over time. Constellation continuously looks to optimize its portfolio of brands to take advantages of the broad trends within the beverage industry.

While Constellation has many brands and does deals within all three beverage categories, it’s best to focus on the Mexican beer business (and its two most popular brands – Corona and Modelo), which is the crown jewel of the company. Corona has many sub-brands like Extra, Light, Premier, Familiar, Refresca and now Hard Seltzer. In FY21, the company sold 154M (+3% y/y) cases of …