AGB 2021.10 - Atlassian (TEAM)

A Sales Efficient Software Company

Subscribe to AGB - One analysis of a good business every two weeks.

Atlassian

“Our mission is to unleash the potential of every team.” - 2020 Annual Report

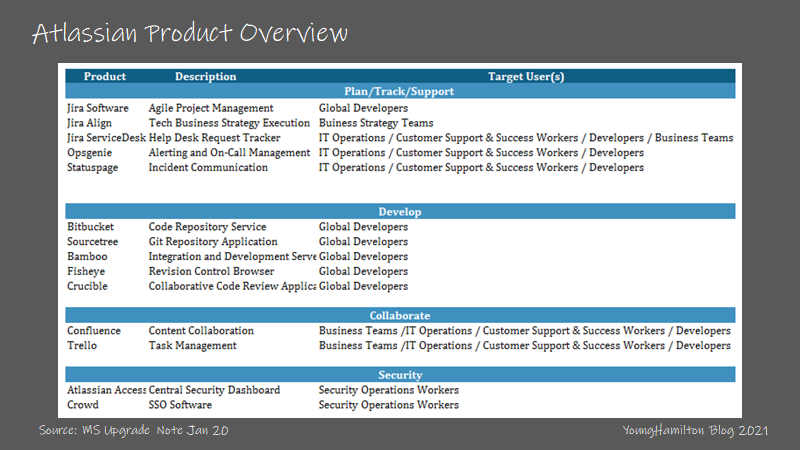

Atlassian is a leading provider of work productivity software. The company’s main products are Jira, Jira Core, Confluence, Trello, Jira Service Desk, Opsgenie and Bitbucket. Atlassian was one of the first companies to benefit from the shift to agile software development (continuous development through short feedback loops) vs. the waterfall methodology (linear sequences of development). As other teams like HR, operations and marketing move towards an agile work environment, there are Atlassian products for each type of team.

There are many other work productivity software companies out there like Asana, Smartsheet, Basecamp, Monday.com, etc., which could imply that this segment of software isn’t as attractive as verticalized software due to the competitive dynamics, but it’s hard to ignore Atlassian’s success and unique history/operat…