AGB 2020.7 - Tyler Technologies (TYL)

Verticalized Software but with Underlying Market Growth

The Update to this initial write-up was posted on April 2025. The financial model can be found near the end of the update post.

Tyler Technologies

Tyler Technologies is the leading software vendor that focuses solely on the public sector in the U.S. At first glance, the growth and/or margin profile of the company may not seem as exciting as other high growth enterprise SaaS companies. But to fully appreciate the unique opportunity at Tyler, one must first understand the nuances of the public sector.

There are three main distinctions when selling to a public sector software customer:

(1) Most deals are a “rip and replace” of systems that are over 30 years old. The Bloomberg article, “America’s Cities Are Running on Software From the ’80s” published in February 2019 said it best.

“The only place in San Francisco still pricing real estate like it’s the 1980s is the city assessor’s office. Its property tax system dates back to the dawn of the floppy disk.”

(2) Public sector customers are not profit motivated but rather just want things to work. Frequently they rely on recommendations from other customers about which vendors are best suited for their needs. Tyler mentions that the main driving forces behind winning new deals are references from other government agencies that have successfully transitioned to Tyler software. Furthermore, having a complete suite of offerings that meets many different sub agencies’ needs can boost win rates.

(3) Budgeting is critical and oftentimes capex and opex come from different sources. This is from the same Bloomberg article.

“For local officials throughout the country, the shift from old-school servers to rented cloud storage has made it tougher than ever to fund upgrades. They can budget physical equipment as capital expenses, meaning they could issue bonds to pay for them. But cloud computing is a service, as the people selling it love to say, which means officials have to pay for it with operating funds—the same pool of money that goes toward addressing more tangible demands, such as parks and cops.”

Tyler has a product in almost every category that addresses the needs of the public sector. The company’s core offerings include ERP, Courts and Justice, e-Filing, Public Safety, Appraisal and Tax, Corrections, Civic Services, etc. to name a few. Tyler’s core customers have been local government agencies which make up 85% of the company’s revenues. State government agencies represent 10% and Federal agencies, which is a new customer set with the recent acquisition of Micropact, represent 5% of revenue.

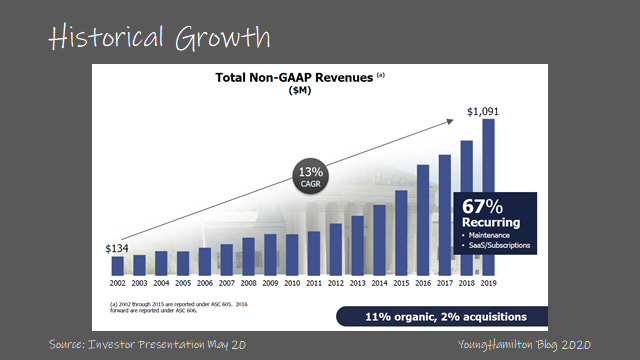

The public sector software market grows at a nice rate of 7%-8% annually and more than 2/3 of the addressable market are greenfield opportunities. Over the past 20 years, Tyler has grown its top line by an average rate of 13%, of which 11% was organic – outpacing the industry. Only 2% of annual growth came from acquisitions, and given Tyler’s plentiful acquisition history, this implies that the acquired businesses also benefited from years of growth after being integrated into the Tyler platform.

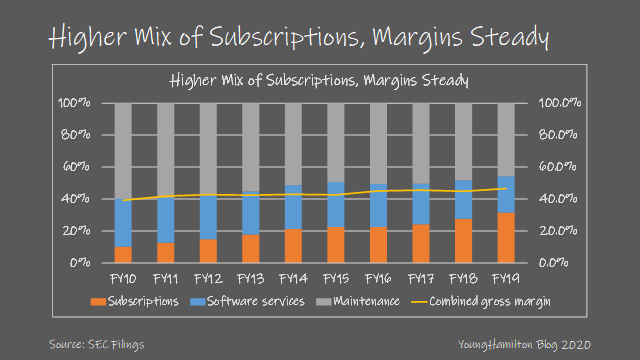

Because public sector budgets for capex and opex are usually separate, Tyler has been agnostic about the way customers have purchased software. The company offers the traditional model of license + maintenance (on-premise) and a subscription (SaaS) model, which is cloud based software run on Tyler’s data centers. The company is more than happy letting customers choose which offering is better suited to fit their needs and budgets.

Even with this agnostic approach, recurring revenue has consistently been a large part of the company’s revenue stream. This is because maintenance revenues for Tyler are almost SaaS like. Tyler sells its software in an evergreen model, meaning that there is only a one time license fee and as long as the customer has a maintenance contract with Tyler, future licenses will not be required for upgrades. Thus, the customer always has the latest version of the software. Since FY10, recurring revenue growth has outpaced non-recurring by a factor of 2x (18% vs. 9% CAGR). In FY10, recurring revenues were just over 55% of total revenues. By FY19, it’s more than 2/3 of total revenues.

Why is it a good business?

Software (and SaaS in particular) is one of the best business models if growth is high and scale can be achieved. Write code once and sell it many times with almost zero marginal cost. Sure, there are hosting costs for cloud software and updates required to maintain product leadership, but generally, margins are very high in software.

Similar to most other software vendors, once a customer is fully up and running on Tyler’s software stack, there are major switching costs. It’s not without reason that the majority of the systems that Tyler itself is displacing are over 30 years old. The initial cost to implement the software and then train people how to use the software is high. Then as the customer uses the software over time, more processes and protocols rely on the software so that it becomes almost indispensable. Only after many years of the software being outdated, does the customer finally relent and replace the entire system.

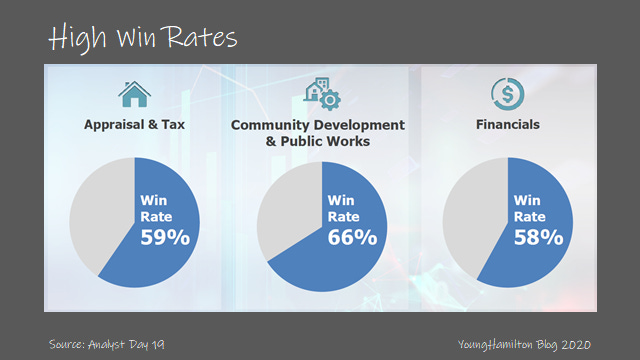

Tyler’s model also exhibits economies of scope. Tyler, with its comprehensive suite of offerings and its strong reputation among public sector customers, has the best win rates in the industry. Now, it’s debatable whether scope is actually a competitive advantage, but hear us out. We think it actually does provide a benefit and a barrier in this case. Because public sector customers are not profit driven but rather trying to improve efficiency within the framework of annual budgets, having a variety of offerings that integrate well with one another allows Tyler to win more deals. That’s a long way of saying that offering software solutions that allows courts to connect with police agencies, and also process e-filing, e-warrants, e-citations and offer case management results in best in class win rates above 85%.

Tyler’s win rates are strong in a number of other offerings as well. Appraisal and Tax win rates are 59%, Community Development and Public Works 66% and Financials 58%. Within Public Safety, of which New World Systems is the largest part, win rates have gone from 25%-30% prior to the Tyler acquisition in 2015 to over 50%. Win rates above 50%, if you assume that Tyler gets a look at most deals, implies that Tyler is taking market share.

These advantages and Tyler’s strong commitment to improving its product offerings over time have resulted in very high customer retention rates of 98%-99%.

The recurring nature of Tyler’s business model is also an advantage. Tyler’s backlog has consistently increased as the company has grown its top line. Backlog at year end are contracts that have been signed but revenue has yet to be recognized. At the end of FY19, Tyler had a backlog that was 134% of the total revenues recognized that year. The backlog/revenues ratio has consistently been between 110% and 145% at year end. Heading into FY20, the company expects to recognize 50% of its backlog of $1.46B during FY20. The growth of SaaS vs. on-premise should help as recurring revenues become an even larger part of total revenues.

Returns on capital?

Tyler has a great track record of allocating capital over the past decade. In those 10 years, Tyler has spent 3.5% of revenues on capex and 5.7% on R&D. Capex is mainly used for Tyler’s data centers where the company hosts its cloud based software offerings. R&D is mainly for software development. Tyler has spent 12% of its revenues on acquisitions and many have been homeruns.

When making acquisitions, Tyler is judicious on price and always considers the build vs. buy comparison. The company typically pays between 6x-7x EBITDA for companies with traditional license + maintenance models, which implies a return of 14%-17% on these deals. Keep in mind this is before any future growth, which may significantly improve the return (and lower the multiple). After an acquisitions is made, Tyler integrates the offering onto its platform and typically scales the business over time.

For example, the company acquired New World Systems for $700M (largest in Tyler’s history) in FY15 to address a need in Public Safety. The company then launched development projects to enhance the competitiveness of the product that would better position the product in higher tier markets. Tyler also integrated New World Systems with its Courts & Justice product as a complementary offering. Win rates have improved from 25%-30% at the time of acquisition to over 50%. Other examples of successful growth after acquisition include Wiznet ($9M acquisition) in FY10 and Brazos ($6M) in FY15.

Tyler’s recent large deals include Socrata ($150M) in FY18 and Micropact ($195M) in FY19. Tyler paid 5x forward revenues for Socrata since it’s a SaaS offering with little reportable earnings and 12x-13x EBITDA (2.5x revenue) for Micropact. While Tyler did pay more for Micropact than the company typically wants to pay, Tyler got a nice entryway into the Federal segment of public sector. Micropact has installations in over 90% of federal agencies.

With each acquisition, the addressable market for Tyler grows larger. In FY17, the company stated that its TAM was $7B currently addressable and $13B in total. The TAM estimates are $9B currently addressable and $21B total as of FY20.

Tyler has flexed R&D spend up in the past few years as acquisition multiples have increased with the market. The company has mentioned that private equity sources are driving up deal multiples.

With the core business growing organically between 10%-12% and acquisitions returning 14%-17% before any improvements, we estimate that total return on capital is somewhere in the range of 25%-30% for the company. Remember, that Tyler participates in a market that is growing 7%-8% annually, it’s easy to increase the return on acquisitions as long as Tyler pays a reasonable multiple.

Reinvestment potential?

The growth opportunity remains large for Tyler even within the local governments segment. Tyler estimates that there are over 450k system opportunities of which Tyler currently has over 26,000 installations or 5.8% of the market. The company estimates that 1/3 of these potential customers have competitive vendor software installed but 2/3 still remain on unsupported or home grown systems. Within specific products, Tyler estimates that they have 14% share in Appraisal & Tax, 7% share in Community Development & Public Works and 17% in Financials.

e-Filing is another large potential opportunity for the company. Courts and other government agencies around the U.S. are filing more of their documents via e-Filing. Tyler is by far the leading player in this space, with 16 state wide e-Filing arrangements as of FY18. Tyler typically receives a transaction based fee per filing similar to many other e-Filing competitors’ solutions.

In the near-term, Tyler estimates that there is still ample room to expand relationships with existing clients and win new opportunities within all of its product categories. Furthermore, as the company sells more cloud based deals in the future, Tyler should extract more value out of the market as the life time value of SaaS customers are 2x that of on-premise. Tyler also has an opportunity to move up market to go after more State and Federal deals, but this will be met with some pushback from the other large software vendors that don’t solely focus on the government vertical like Oracle, SAP and Infor.

Tyler can accelerate its penetration into its many end markets with future acquisitions. As mentioned before, the company has taken a pause to making large acquisitions in the recent year to focus on integrations of Socrata and Micropact. Multiples in the space have increased as well, making the hurdle rates for acquisitions more difficult to achieve. However, the company has recently noted that the recent environment may have created some additional opportunities to do deals.

We estimate that Tyler has reinvested between 50%-60% of its capital over the past 5 years, with returns ranging between 25%-30%. This implies that intrinsic value has compounded at a rate between 13%-17% annually, very well within the range of being a good business.

What else is important?

More SaaS than on-premise

In the past year or so, Tyler has noted that its customers have been more inclined to choose its SaaS offering vs. on-premise. Typically, a shift in mix from on-premise to SaaS lowers revenue growth but improves cash flow. Many investors already know this to be the case and we’ve seen many successful transitions like Adobe, Microsoft and Intuit to name a few.

We would like to point out that in Tyler’s case, the benefit will not be as pronounced for two reasons. First, because Tyler sells its license software as evergreen, there are no subsequent license revenue contributions after the initial purchase from a customer. This implies that maintenance revenues is a larger portion of total life time value of a customer, which makes Tyler’s on-premise offering already SaaS like. Second, Tyler’s software is generally single tenant instead of multi-tenant. This means that each customer is running their own instance of the software on Tyler’s cloud servers, which provides fewer scale advantages as the SaaS offering gets larger.

So instead of seeing much better cash flow growth and incremental margin expansion over time after an initial dip (what is typical of on-prem to SaaS transition), Tyler will mainly benefit from better LTV (typically 2x the revenue) but less than 2x the profits (margins don’t really expand enough and there are hosting costs). Tyler’s partnership with Amazon AWS may help with making some of software to become more multi-tenant like and lower hosting costs, which should boost margins over time. This transition will be a 2 to 5 year process.

Competition from Central Square

Central Square has emerged as a significant competitor to Tyler within Public Safety and ERP. The company was formed by merging a collection of subsidiaries of Vista Equity Partners and Bain Capital. TriTech Software, Superion (Sunguard), Zuercher and Aptean merged together to form this new entity in 2018.

Central Square has less scope in-terms of product offering and geographic relevance. Competition from Central Square could have a negative impact to Tyler’s win rates, especially in certain geographies that Central Square has a larger presence. We need to keep an eye on this new entrant to make sure that there isn’t a meaningful impact to revenue growth or win rates.

Optionality

Meaningful acquisition

We can envision three reasonable call options for the company in Tyler’s future. The first is another meaningful acquisition. Tyler has been acquisitive in the past two years and the company did mention at the end of FY19 and earlier this year that the company would take some time to focus on integration before looking to do more large deals. Covid and everything else this year made it more difficult to find new acquisitions. As generalists, it’s difficult to put together a list of potential targets, but given that the market is still very underpenetrated, Tyler has the luxury of paying a little bit more for acquisitions than software vendors targeting other markets.

International

Tyler has a small presence internationally, which comprises 3% of total revenues. The company has yet to make it a top priority, given the ample opportunity left in the U.S. public sector. Currently, increasing the company’s penetration into the State and Federal market is lower hanging fruit. However, there isn’t anything precluding the company from International expansion. The caveat to think about is how much product leverage there can be across different countries. Even if there are a lot of common features and functions that can be shared between geographies, building a sales organization to grow in International markets will be margin dilutive, at least initially.

Tyler Payments

The most interesting call option is in payments. The company has mentioned its Tyler Payments initiative publicly before on a few earnings calls. Currently, the company does about $7M per quarter in payments, mostly through collecting a small percentage of the payments for traffic tickets and utility bills.

Many government entities that face the public like courts, public safety, appraisals & tax, DMV, etc., have disparate payment systems in place. One of Tyler’s goals is to unify all these payment methods into one central service and then leverage the payment volume to better negotiate processing rates for its customers. This would essentially make Tyler a merchant processor that deals with the networks and the different banking institutions. Tyler envisions that it would get a small percentage of the transaction for this service.

If you made it this far, I hope you received some value from reading our analysis. Please subscribe to the free newsletter (if you haven’t already) and share with anyone that would find it valuable. Thank you for your support!

does the fact that the end customer (government) not have a profit motive affect Tyler downstream in pricing negotiations and growth rate? what if gov budget needs to go into austerity?