Subscribe to AGB - One analysis of a good business every two weeks.

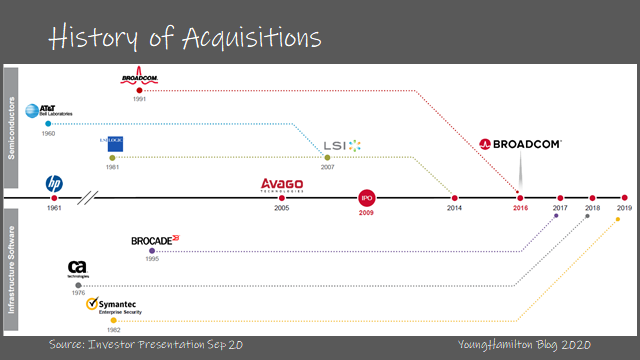

Broadcom/Avago

To limit confusion, we’ll call the company Avago and only refer to Broadcom as the company that Avago acquired in 2016. Avago acquired Broadcom and then took on the name.

Avago is the fourth largest semiconductor company by revenues after Intel, SK Hynix and Qualcomm. The company was formed in 2005 when the semiconductor division of Agilent was sold to private equity firms, KKR and Silver Lake Partners. Shortly after in early 2006, Hock Tan was brought in as CEO. The company went public in 2009 and at the time was much smaller in size and scope as compared to today.

Avago has grown mainly through a series of acquisitions starting in late 2014 with the acquisition of LSI. Subsequent to that acquisition, Avago has made one major acquisition per year, integrating these new companies with speed and efficiency. The second most impactful acquisition was Broadcom in 2016, which at the time was actually 30% larger …